2026 Social Security COLA: 3.2% Increase & Your Benefits

The 2026 Social Security Cost-of-Living Adjustment: How a 3.2% Increase Impacts Your Benefits

The financial landscape for millions of Americans relying on Social Security is constantly evolving, with the annual Cost-of-Living Adjustment (COLA) playing a pivotal role in maintaining their purchasing power. As we look ahead, projections for the Social Security COLA 2026 suggest a 3.2% increase. This anticipated adjustment is a critical piece of information for retirees, disabled individuals, and survivors, as it directly influences the amount of their monthly benefits. Understanding the mechanics behind this adjustment, its potential impact, and how to prepare for it is essential for effective financial planning in the coming years. This comprehensive guide will delve into the intricacies of the 2026 COLA, explaining its calculation, its historical context, and the broader implications for your financial well-being.

For many, Social Security benefits represent a significant, if not primary, source of income. Therefore, any adjustment, whether up or down, carries substantial weight. A 3.2% increase, while not as dramatic as some recent years, still signifies a meaningful boost designed to help beneficiaries keep pace with inflation. However, the real-world effect of this increase can vary widely depending on individual circumstances, including Medicare premiums, taxes, and other financial obligations. Our aim is to provide clarity on these complex issues, empowering you to make informed decisions about your retirement and financial future.

Understanding the Social Security COLA: A Foundation for 2026

Before we dive into the specifics of the Social Security COLA 2026, it’s crucial to understand what the COLA is and why it exists. The Cost-of-Living Adjustment is an annual increase in Social Security and Supplemental Security Income (SSI) benefits. Its primary purpose is to protect the purchasing power of beneficiaries from the effects of inflation. Without COLA, the fixed income of retirees and other beneficiaries would gradually lose value over time, making it harder to afford essential goods and services.

The Social Security Act mandates that COLAs be calculated based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the Social Security Administration (SSA) compares the average CPI-W for the third quarter of the current year (July, August, and September) with the average for the third quarter of the last year in which a COLA was payable. The percentage increase between these two periods determines the COLA. If there is no increase, then no COLA is applied for that year.

This method ensures that benefits adjust to reflect changes in the cost of living, theoretically allowing beneficiaries to maintain their standard of living. However, the CPI-W is not without its critics. Some argue that it doesn’t accurately reflect the spending patterns of seniors, who often spend a larger proportion of their income on healthcare costs, which tend to rise faster than other goods and services. Despite these criticisms, the CPI-W remains the statutory basis for COLA calculations.

The COLA is typically announced in October each year, based on the inflation data from the third quarter. The adjustment then takes effect in December, with the increased benefits appearing in payments starting in January of the following year. So, the 2026 COLA, based on 2025 inflation data, will be announced in October 2025 and implemented in January 2026.

The Projected 3.2% Increase for Social Security COLA 2026: What Does it Mean?

The projection of a 3.2% increase for the Social Security COLA 2026 is a significant figure that anticipates ongoing inflationary pressures, albeit potentially at a more moderate pace than in recent years. To put this into perspective, let’s consider what a 3.2% increase could mean for an average beneficiary. If an individual is currently receiving $1,800 per month in Social Security benefits, a 3.2% COLA would translate to an additional $57.60 per month, bringing their new monthly benefit to $1,857.60.

While this might seem like a modest increase, over the course of a year, it adds up to an extra $691.20. For those living on fixed incomes, this additional amount can make a tangible difference in covering rising costs for groceries, utilities, and other necessities. However, it’s important to remember that this is a projection, and the final COLA will depend on the actual CPI-W data for the third quarter of 2025.

The 3.2% projection reflects a scenario where inflation continues to be a factor in the economy, but perhaps not at the same elevated levels seen during the peak of recent inflationary cycles. Economic forecasts often consider various factors, including global supply chain dynamics, energy prices, wage growth, and consumer demand, all of which contribute to the overall inflation rate. A 3.2% COLA suggests that economists anticipate these factors will continue to push prices upward, necessitating an adjustment to Social Security benefits.

It’s also crucial to consider how this projected COLA compares to historical adjustments. Over the past decade, COLAs have fluctuated significantly. Understanding these historical trends can provide valuable context for the 2026 projection and help beneficiaries gauge its impact on their long-term financial planning.

Historical Context of Social Security COLAs: Trends and Patterns

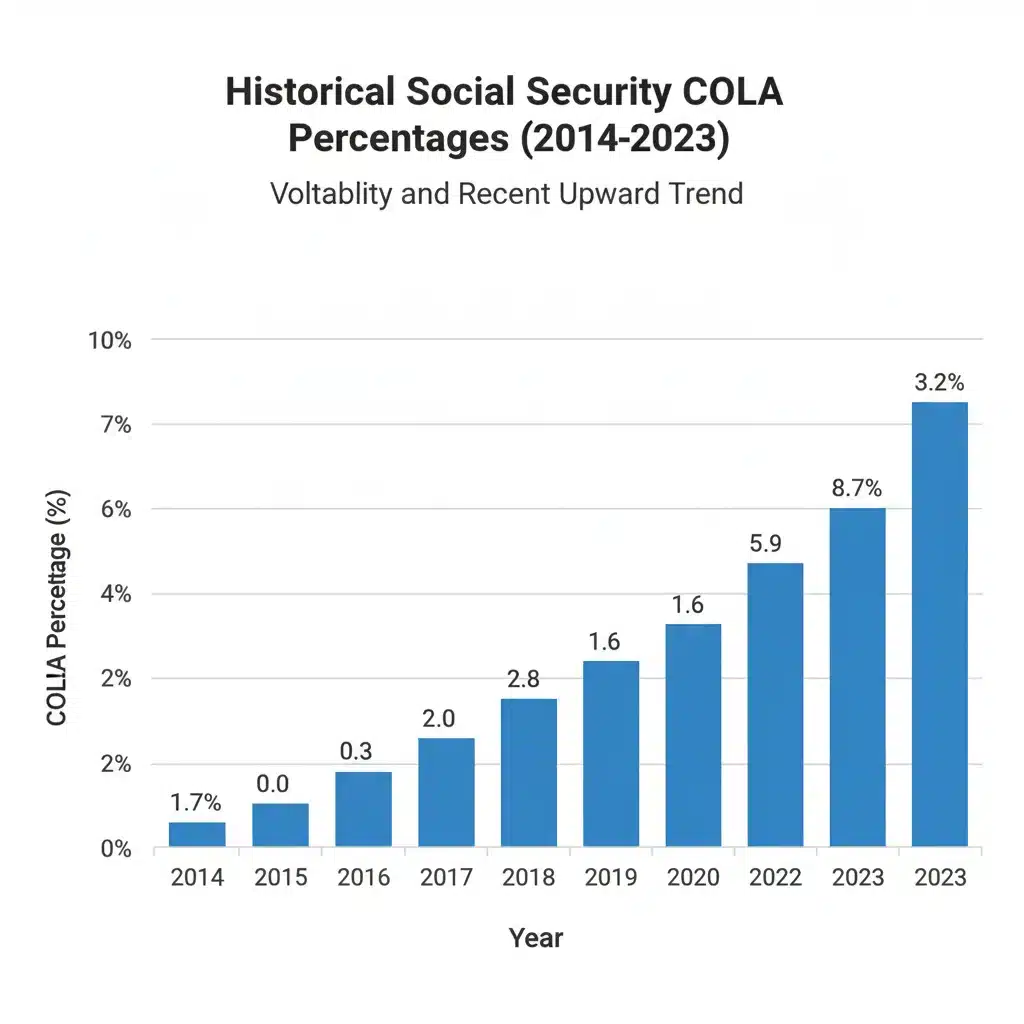

Examining past Social Security COLA adjustments provides valuable insight into the volatility of inflation and its direct impact on beneficiaries. While the projected 3.2% for 2026 is noteworthy, it’s useful to compare it with previous years to understand the broader trends. In recent history, we’ve seen a wide range of COLAs, from years with no increase to significant jumps.

For instance, in 2022, beneficiaries received a substantial 5.9% COLA, followed by an even larger 8.7% COLA in 2023, reflecting unprecedented levels of inflation. These larger adjustments were crucial for helping seniors cope with rapidly rising prices for everyday goods and services. Prior to these high-inflation years, COLAs were generally more modest, often in the 0% to 2% range, and there were even years, such as 2010, 2011, and 2016, where no COLA was applied due to low or negative inflation as measured by the CPI-W.

The fluctuating nature of COLAs underscores the importance of not relying solely on these adjustments for financial stability. While they are designed to preserve purchasing power, they are reactive to inflation rather than proactive. This means that beneficiaries often feel the pinch of rising prices before the COLA takes effect, and the adjustment might not fully compensate for all personal expenses, especially those with higher inflation rates like healthcare.

Analyzing these historical patterns reveals a cyclical nature influenced by broader economic conditions. Periods of economic growth and higher demand often lead to increased inflation and consequently higher COLAs. Conversely, economic downturns or periods of stable prices result in lower or non-existent adjustments. The 3.2% projection for the Social Security COLA 2026 suggests a return to a more moderate inflationary environment compared to the peaks of 2022 and 2023, but still a recognition of persistent price increases.

Understanding these trends helps beneficiaries contextualize the upcoming adjustment and plan accordingly. It reinforces the idea that while COLA is a vital safeguard, a well-rounded retirement plan should include diversified income sources and strategies to mitigate the impact of inflation beyond Social Security benefits.

The Impact of the 3.2% COLA on Your Monthly Benefits

A 3.2% increase in the Social Security COLA 2026 directly translates to a higher monthly benefit payment. However, the net impact on your take-home amount can be influenced by several factors, most notably Medicare premiums and income taxes. It’s not as simple as just adding 3.2% to your current check.

Medicare Premiums and the ‘Hold Harmless’ Provision

For many Social Security beneficiaries, Medicare Part B premiums are deducted directly from their monthly benefit checks. These premiums also tend to increase annually. The ‘hold harmless’ provision is a crucial protection for many beneficiaries: it prevents their net Social Security benefit from decreasing due to an increase in Medicare Part B premiums. If your Medicare Part B premium increase is greater than your COLA, the ‘hold harmless’ provision ensures that your premium increase is capped at the amount of your COLA, so your actual cash benefit doesn’t go down. However, this provision primarily applies to those who have their Part B premiums deducted from their Social Security checks and do not pay an income-related monthly adjustment amount (IRMAA).

If you are new to Medicare, pay higher premiums due to IRMAA, or do not have your premiums deducted from Social Security, you may not be fully protected by ‘hold harmless’. This means that even with a 3.2% COLA, your net increase might be partially or fully offset by rising Medicare costs.

Income Taxes on Social Security Benefits

Another significant factor is the taxation of Social Security benefits. Depending on your ‘provisional income’ (which includes your adjusted gross income, tax-exempt interest, and half of your Social Security benefits), a portion of your Social Security benefits may be subject to federal income tax. An increase in your benefits due to the 3.2% COLA could, for some individuals, push their provisional income past certain thresholds, leading to a higher percentage of their benefits being taxable.

For single filers, if your provisional income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If it’s over $34,000, up to 85% may be taxable. For married couples filing jointly, these thresholds are $32,000 and $44,000, respectively. While a 3.2% COLA might not drastically change your tax bracket, it’s a factor to consider, especially if your income is close to these thresholds. State income taxes are another potential consideration, as some states also tax Social Security benefits.

Therefore, while the 3.2% COLA is a welcome boost, the actual take-home increase for beneficiaries will depend on their individual financial situation, including Medicare costs and tax obligations. It underscores the importance of reviewing your overall financial picture annually.

Strategies to Maximize Your Benefits and Prepare for the 2026 COLA

Understanding the projected 3.2% Social Security COLA 2026 is just the first step. Proactive planning can help you maximize the impact of this increase and ensure your financial security in retirement. Here are several strategies to consider:

1. Review Your Budget and Expenses

With an anticipated increase in benefits, now is an excellent time to review your current budget. Identify areas where costs have risen due to inflation and assess how the COLA might help offset these increases. This review can also highlight areas where you might be able to cut back or find more cost-effective alternatives, further stretching your Social Security income. Pay particular attention to rising healthcare costs, which often outpace general inflation.

2. Understand Medicare Premium Changes

As discussed, Medicare Part B premiums can significantly impact your net Social Security benefit. Stay informed about the projected Medicare premium increases for 2026. If you are not protected by the ‘hold harmless’ provision, or if you pay IRMAA, understanding these changes early can help you adjust your budget accordingly. Explore options like Medicare Advantage plans or Medigap policies to see if you can optimize your healthcare spending.

3. Consider the Taxation of Benefits

If your income is close to the federal thresholds for taxing Social Security benefits, a 3.2% COLA could potentially push you into a higher taxable bracket. Consult with a tax advisor to understand the implications for your specific situation. Strategies like tax-efficient withdrawals from retirement accounts (e.g., Roth conversions) or managing other sources of income can help minimize your tax liability on Social Security benefits.

4. Delaying Social Security (If Applicable)

For those who are not yet claiming Social Security benefits, delaying your claim beyond your full retirement age (up to age 70) can significantly increase your monthly payments. Not only do you receive delayed retirement credits, but these higher initial benefits are then subject to future COLAs. A 3.2% COLA on a larger initial benefit will result in a more substantial dollar increase compared to applying it to a smaller, earlier claimed benefit.

5. Explore Additional Income Streams

While Social Security provides a vital foundation, relying solely on it can be risky, especially in times of fluctuating inflation. Consider exploring additional income streams in retirement, such as part-time work, dividends from investments, rental income, or drawing from personal savings. A diversified income portfolio provides greater financial resilience and reduces dependence on COLA adjustments alone.

6. Re-evaluate Your Investment Strategy

For those with investment portfolios, regularly review your strategy to ensure it aligns with your retirement goals and risk tolerance. Consider investments that offer some protection against inflation, such as Treasury Inflation-Protected Securities (TIPS) or real estate. A well-managed investment portfolio can supplement your Social Security income and help maintain your purchasing power over the long term, regardless of the annual COLA.

7. Stay Informed and Seek Professional Advice

The rules and projections surrounding Social Security can be complex and are subject to change. Stay updated on official announcements from the Social Security Administration and economic forecasts. Don’t hesitate to seek advice from qualified financial advisors who specialize in retirement planning. They can provide personalized guidance tailored to your unique circumstances, helping you navigate the intricacies of Social Security and other retirement income sources.

The Broader Economic Picture and Future COLA Projections

The projected 3.2% Social Security COLA 2026 is not an isolated figure; it’s a reflection of the broader economic environment. Several economic factors influence inflation and, consequently, the COLA. Understanding these factors can provide a clearer picture of what to expect in the coming years.

Inflationary Pressures

The primary driver of COLA is inflation. Factors contributing to inflation include:

- Supply Chain Dynamics: Disruptions in global supply chains can lead to higher production costs and increased consumer prices. While some supply chain issues have eased, new geopolitical events or natural disasters could reignite these pressures.

- Energy Prices: Fluctuations in oil and gas prices have a ripple effect throughout the economy, impacting transportation costs for goods and services, and directly affecting household budgets.

- Wage Growth: Strong wage growth can contribute to increased consumer spending, which in turn can push prices higher. While beneficial for workers, sustained high wage growth without corresponding productivity gains can fuel inflation.

- Consumer Demand: High consumer demand, often bolstered by a strong job market and fiscal stimuli, can give businesses the ability to raise prices.

- Monetary Policy: Actions taken by central banks, such as interest rate adjustments, aim to control inflation. The effectiveness of these policies in achieving price stability directly impacts future COLA calculations.

The 3.2% projection suggests that economists expect these factors to continue exerting some upward pressure on prices, but perhaps not at the same intense level as seen in the immediate post-pandemic period. This indicates a potential stabilization of inflation, moving towards more historical averages, though still above the Federal Reserve’s long-term target of 2%.

Impact of Economic Growth and Recession Risks

The state of the economy also plays a crucial role. A robust economy with strong employment generally leads to higher consumer spending and potential inflation. Conversely, an economic slowdown or recession could lead to subdued inflation or even deflation, which would result in lower or no COLA. Forecasters constantly weigh the risks of recession against continued growth when making COLA projections.

Long-Term Outlook for Social Security

Beyond the annual COLA, it’s important to consider the long-term solvency of the Social Security program itself. While COLAs help current beneficiaries, the broader financial health of Social Security is a topic of ongoing discussion and concern. Demographic shifts, such as lower birth rates and increased life expectancies, mean fewer workers are contributing per beneficiary. Understanding these long-term challenges is essential for a complete picture of Social Security’s future and its ability to provide benefits, including COLAs, for generations to come.

The 2026 COLA, therefore, is not just a number; it’s a reflection of complex economic forces at play. Keeping an eye on these broader trends can help beneficiaries and future retirees better anticipate and plan for their financial futures.

Conclusion: Preparing for Your Financial Future with the 2026 COLA

The projected 3.2% Social Security COLA 2026 is a critical piece of information for millions of Americans who depend on these benefits. While it represents a positive adjustment designed to combat inflation, its actual impact on your personal finances will depend on a confluence of factors, including Medicare premiums, potential tax implications, and your overall financial strategy. It’s clear that understanding the mechanics of COLA, its historical context, and the broader economic landscape is paramount for effective retirement planning.

The journey to financial security in retirement is ongoing, and the annual COLA is just one component. By proactively reviewing your budget, understanding healthcare costs, planning for taxes, and exploring supplementary income streams, you can position yourself to make the most of the 2026 COLA and any future adjustments. Remember that personalized financial advice can be invaluable in navigating these complexities and tailoring strategies to your unique circumstances.

As we move closer to the official announcement of the 2026 COLA in October 2025, staying informed and prepared will be your best defense against economic uncertainties. Embrace a holistic approach to your retirement planning, ensuring that Social Security, enhanced by annual COLAs, remains a strong and reliable pillar of your financial well-being.