Securing Your Future: Navigating the 2026 Social Security Trust Fund Outlook

Securing Your Future: Navigating the 2026 Social Security Trust Fund Outlook

The year 2026 might seem distant, but for millions of Americans, it represents a critical juncture for the future of their retirement. The Social Security Trust Fund, a cornerstone of financial security for the elderly, disabled, and survivors, faces significant challenges that demand our attention and proactive solutions. Understanding the Social Security Future is not just for policymakers; it’s a vital exercise for every individual planning their retirement.

For decades, Social Security has provided a safety net, ensuring a basic level of income for those who can no longer work. However, demographic shifts, including lower birth rates and increased life expectancy, coupled with economic fluctuations, have placed increasing pressure on the system. The projections for the Social Security Trust Fund in 2026 are a wake-up call, prompting an urgent need to explore practical solutions to secure these crucial benefits for generations to come.

This comprehensive guide will delve into the intricacies of the 2026 Social Security Trust Fund outlook. We’ll break down what these projections mean for you, explore the underlying causes of the challenges, and, most importantly, provide actionable strategies and potential solutions to strengthen the system and safeguard your Social Security Future. Whether you’re nearing retirement, just starting your career, or somewhere in between, understanding these dynamics is paramount to making informed financial decisions.

Understanding the Social Security Trust Fund: A Primer

Before we dive into the 2026 outlook, it’s essential to grasp the fundamentals of how Social Security works. Social Security is primarily funded through payroll taxes, specifically the Federal Insurance Contributions Act (FICA) and the Self-Employment Contributions Act (SECA) taxes. These taxes are collected from employees, employers, and self-employed individuals. The revenue generated is then used to pay current beneficiaries. Any surplus funds are invested in special U.S. Treasury securities, held by the Social Security Trust Funds.

There are two primary Social Security Trust Funds:

- Old-Age and Survivors Insurance (OASI) Trust Fund: This fund pays retirement and survivor benefits.

- Disability Insurance (DI) Trust Fund: This fund pays disability benefits.

While often discussed together, these two funds are legally separate. Historically, they have been able to borrow from each other to cover shortfalls, but the overall health of both funds is crucial for the long-term solvency of the Social Security program. The trustees of Social Security release annual reports detailing the financial status and projections of these funds. These reports are what inform the discussions and concerns surrounding the Social Security Future.

The concept of a ‘trust fund’ can sometimes be misleading. It’s not a vault full of cash waiting to be disbursed. Instead, it represents the government’s obligation to pay future benefits, backed by these special Treasury securities. When Social Security collects more in taxes than it pays out in benefits, the surplus is invested. When it pays out more than it collects, it redeems these securities. The problem arises when the system consistently pays out more than it collects, leading to a depletion of these reserves.

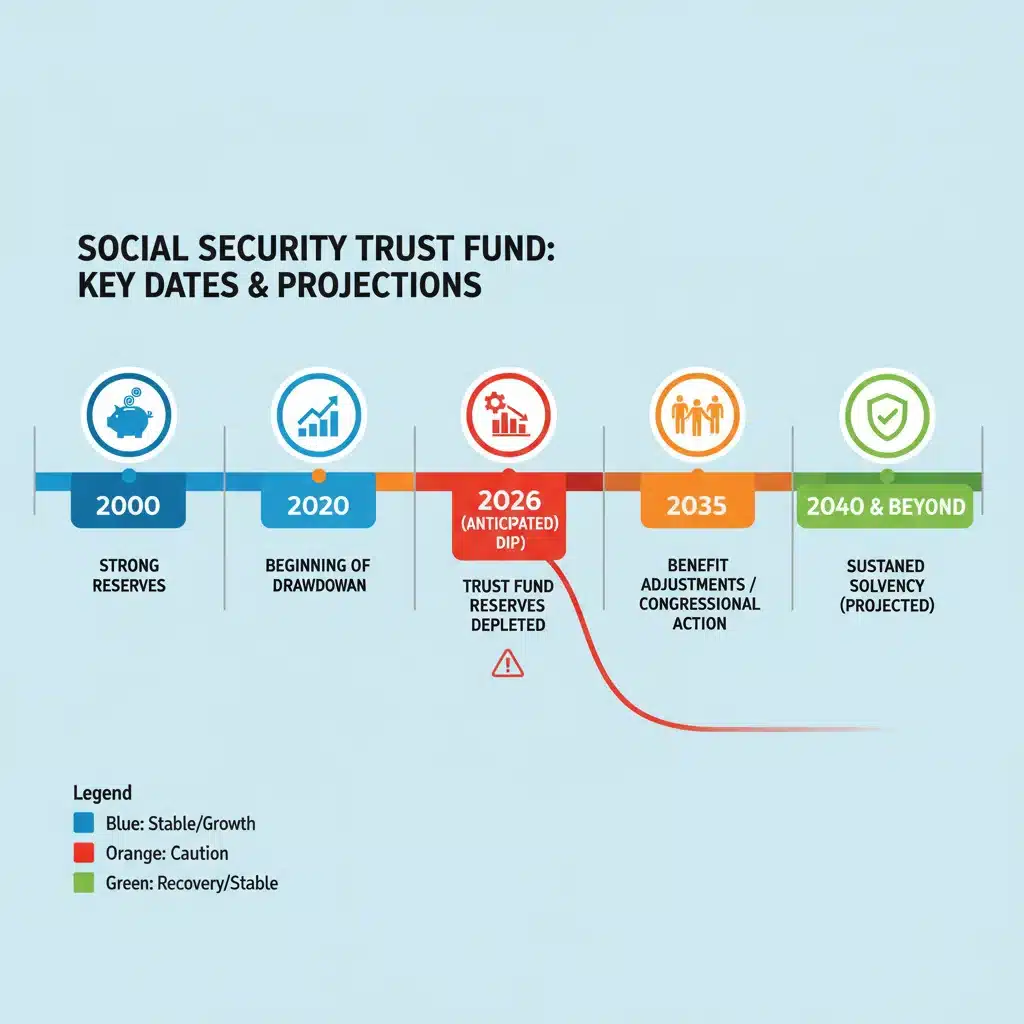

The 2026 Outlook: What the Projections Say

The latest Social Security Trustees’ Report has highlighted a significant milestone approaching in 2026. While the specific date can shift slightly with each annual report due to updated economic and demographic assumptions, the general trend remains consistent: the Social Security Trust Fund is projected to begin drawing down its reserves at an accelerated pace. This means that, without legislative action, the program will eventually be unable to pay 100% of promised benefits.

Specifically, the OASI Trust Fund is projected to be able to pay 100% of scheduled benefits until a certain point, after which it will only be able to pay a reduced percentage. The DI Trust Fund has a different trajectory but also faces long-term solvency issues. The combined OASI and DI Trust Funds are projected to be able to pay 100% of scheduled benefits until approximately the mid-2030s, after which they would only be able to pay around 80% of scheduled benefits if no changes are made. The year 2026 is often cited as a critical point because it marks the beginning of a more rapid decline in the trust fund’s reserves, signaling a shorter window for legislative intervention before more drastic measures might be required.

These projections are not a prediction of Social Security’s collapse. Social Security will not ‘run out of money’ in the sense that it will cease to exist. As long as people are working and paying FICA taxes, revenue will continue to flow into the system, and benefits will continue to be paid. The issue is the ability to pay full scheduled benefits. If no action is taken, future retirees and beneficiaries could face a significant reduction in their expected payments, fundamentally altering their plans for the Social Security Future.

Causes of the Social Security Trust Fund Challenges

Understanding the root causes of the Social Security Trust Fund’s challenges is crucial for formulating effective solutions. It’s not a single factor but a confluence of demographic, economic, and policy trends:

Demographic Shifts: Fewer Workers, More Retirees

One of the most significant factors is the changing demographic landscape. The ratio of workers contributing to Social Security to beneficiaries receiving benefits has been steadily declining. This is primarily due to:

- Lower Birth Rates: Fewer children being born means a smaller workforce in the future to support a larger elderly population.

- Increased Life Expectancy: People are living longer, healthier lives, which means they are collecting Social Security benefits for a longer period. While this is a positive societal development, it places greater strain on the system.

- The Baby Boomer Generation: The large cohort of Baby Boomers is now entering or already in retirement, leading to a surge in beneficiaries.

In the mid-20th century, there were many more workers for every retiree. Today, that ratio is much smaller, and it is projected to continue to shrink, exacerbating the funding imbalance for the Social Security Future.

Economic Factors: Wage Growth and Inflation

Economic conditions also play a role. Social Security’s funding is tied to wage growth, as payroll taxes are based on earnings. If wage growth is slow, the tax base doesn’t expand as rapidly as needed. Inflation, while leading to cost-of-living adjustments (COLAs) for beneficiaries, can also impact the purchasing power of the trust fund’s reserves over time if investment returns don’t keep pace.

Policy Decisions and Program Design

Past policy decisions, while well-intentioned, have contributed to the current situation:

- Benefit Formulas: The way benefits are calculated, based on historical earnings, can lead to higher benefits for those with higher lifetime earnings, contributing to overall program costs.

- Retirement Age: While the full retirement age has gradually increased for those born after 1937, it hasn’t kept pace with increases in life expectancy.

- Taxable Earnings Cap: There is a cap on the amount of earnings subject to Social Security taxes. Earnings above this cap are not taxed for Social Security purposes, which some argue limits the program’s revenue.

These intertwined factors create a complex challenge, making it clear that a multi-faceted approach will be necessary to secure the Social Security Future.

Practical Solutions for Securing Your Social Security Future

While legislative action is ultimately required to address the long-term solvency of Social Security, there are practical solutions and strategies that individuals, policymakers, and society as a whole can consider to strengthen the system and protect your benefits.

Individual Strategies: Taking Control of Your Retirement

Even with uncertainty surrounding the Trust Fund, individuals can take proactive steps to secure their own financial future:

- Don’t Rely Solely on Social Security: Treat Social Security as one component of your retirement income, not the sole source. Diversify your retirement savings with 401(k)s, IRAs, and other investment vehicles.

- Save More, Invest Wisely: Increase your personal savings rate and invest in a diversified portfolio aligned with your risk tolerance and time horizon. The earlier you start, the more time your money has to grow through compounding.

- Delay Claiming Benefits (If Possible): For every year you delay claiming Social Security benefits past your full retirement age (up to age 70), your benefit amount increases. This can significantly boost your monthly income in retirement.

- Understand Your Benefit Statement: Regularly review your Social Security statement to ensure your earnings record is accurate and to get an estimate of your future benefits. This helps in personal financial planning for your Social Security Future.

- Consider Working Longer: If feasible, working a few extra years can not only boost your Social Security benefits but also allow you to save more and keep your accumulated savings untouched for longer.

Potential Legislative Solutions: What Policymakers Could Do

Legislators have several levers they can pull to shore up the Social Security Trust Fund. These often involve a combination of increasing revenue and adjusting benefits:

Increasing Revenue:

- Raise the Payroll Tax Rate: A small increase in the FICA tax rate for employees and employers could significantly improve the Trust Fund’s solvency.

- Raise or Eliminate the Taxable Earnings Cap: As mentioned, there’s a cap on earnings subject to Social Security taxes. Raising or eliminating this cap would mean higher earners contribute more to the system.

- Broaden the Tax Base: Some proposals suggest taxing other forms of income, though this is often controversial.

- Invest a Portion of the Trust Fund in Equities: While currently restricted to Treasury securities, some advocate for allowing a small portion of the Trust Fund to be invested in the stock market, potentially yielding higher returns over the long term. This comes with increased risk, however.

Adjusting Benefits:

- Increase the Full Retirement Age: Gradually raising the full retirement age to reflect increased life expectancy would reduce the total amount of benefits paid out over a person’s lifetime.

- Adjust the Cost-of-Living Adjustment (COLA) Formula: Modifying the COLA calculation, perhaps by using a different inflation index (e.g., the Chained CPI), could slow the growth of benefits over time.

- Means-Testing Benefits: This controversial proposal would reduce benefits for higher-income retirees, effectively targeting resources to those who need them most.

- Modify the Benefit Formula: A slight alteration to the formula used to calculate initial benefits could also contribute to savings.

It’s important to note that many of these solutions are politically challenging, as they involve trade-offs and impact different segments of the population. A bipartisan consensus will be essential to implement meaningful reforms for the Social Security Future.

The Role of Economic Growth and Immigration

Beyond direct legislative changes, broader economic and demographic factors can also influence the Social Security Trust Fund’s health. Robust economic growth, for instance, leads to higher wages and more employment, which in turn generates more payroll tax revenue. Policies that foster a strong economy can therefore indirectly support the Social Security Future.

Immigration also plays a significant role. Immigrants, particularly younger immigrants, often enter the workforce and begin paying into Social Security relatively early in their lives. This can help to bolster the worker-to-retiree ratio, providing a demographic boost to the system. Policies related to immigration, therefore, have implications for the long-term solvency of Social Security.

Both sustained economic growth and a healthy rate of immigration can act as natural stabilizers for the Social Security system, easing some of the demographic pressures it faces. These factors, however, are often subject to broader political and economic forces that are beyond the direct control of Social Security policy.

Dispelling Myths and Understanding Realities

The discussion around Social Security is often fraught with misinformation and fear. It’s crucial to distinguish between myths and realities:

- Myth: Social Security will run out of money completely.

Reality: This is highly unlikely. As long as people are working and paying taxes, Social Security will continue to collect revenue and pay benefits. The issue is whether it can pay 100% of scheduled benefits without legislative changes. - Myth: My Social Security taxes are being stolen or wasted.

Reality: Social Security funds are legally separated from the general federal budget. They are used exclusively to pay benefits and administrative costs. Any surplus is invested in special U.S. Treasury securities, which are backed by the full faith and credit of the U.S. government. - Myth: Young people today will receive nothing from Social Security.

Reality: While future benefits may be adjusted, it’s highly improbable that Social Security will cease to exist. It remains a vital program with broad public support. Young people will almost certainly receive benefits, though the exact amount relative to current levels may change.

Understanding these realities helps to foster a more constructive dialogue about the future of Social Security and encourages a focus on practical solutions rather than alarmism. The goal is to ensure the program’s long-term viability and to secure the Social Security Future for all.

The Importance of Bipartisan Cooperation

Addressing the challenges facing the Social Security Trust Fund requires a concerted effort and, crucially, bipartisan cooperation. The issues are complex, and the solutions often involve difficult choices that impact millions of Americans. Historically, major Social Security reforms have been achieved through bipartisan commissions and legislative compromises. The last significant reform occurred in 1983 under President Reagan, demonstrating that it is possible for different political ideologies to come together to safeguard the program.

Moving forward, a similar spirit of collaboration will be essential. Delaying action only makes the necessary adjustments more severe. The closer we get to the projected insolvency dates, the larger the tax increases or benefit cuts would need to be to restore solvency. Therefore, understanding the 2026 outlook serves as a critical call to action for policymakers to engage in serious, good-faith negotiations to find a sustainable path forward for the Social Security Future.

Conclusion: Planning for a Secure Social Security Future

The 2026 Social Security Trust Fund outlook highlights an undeniable reality: the system faces significant financial challenges that require attention. While the program is not on the verge of collapse, proactive measures are necessary to ensure its long-term solvency and guarantee that it can continue to provide essential benefits to future generations.

For individuals, this means taking personal responsibility for your retirement planning. Diversifying your savings, understanding your Social Security benefits, and considering strategies like delaying claims can significantly bolster your financial security. For policymakers, it means engaging in thoughtful, bipartisan discussions to implement a combination of revenue enhancements and benefit adjustments that will put Social Security on a sustainable path.

The Social Security Future is a shared responsibility. By understanding the challenges, dispelling myths, and advocating for practical solutions, we can all contribute to strengthening this vital program. Your vigilance and informed decision-making, both individually and as a member of society, are key to navigating these challenges and ensuring that Social Security remains a pillar of financial stability for years to come.

Don’t wait for a crisis to act. Start planning your retirement strategy today, stay informed about the ongoing discussions surrounding Social Security, and advocate for responsible solutions that protect this invaluable safety net for yourself and for generations to come. The time to secure our Social Security Future is now.