Maximize Your 2026 Retirement: $23,000 401(k) Limit Strategies

The landscape of retirement planning is constantly evolving, and staying ahead of changes is crucial for securing a comfortable future. As we look towards 2026, one of the most significant updates for savers is the projected increase in the 401(k) contribution limit. This adjustment, moving to an estimated $23,000, presents a golden opportunity for individuals to supercharge their retirement funds. Understanding this new 2026 401(k) Limit and how to leverage it effectively can make a substantial difference in your long-term financial health.

Maximizing Your Retirement Savings in 2026: A Deep Dive into the New $23,000 401(k) Contribution Limit

Retirement planning is not merely about saving; it’s about strategic saving. With the expected increase in the 2026 401(k) Limit to $23,000, individuals have an enhanced capacity to build a robust nest egg. This article will explore the implications of this new limit, delve into effective strategies for maximizing your contributions, and provide insights into making informed decisions about your retirement accounts. Whether you’re a seasoned investor or just starting your retirement journey, understanding these changes is paramount.

Understanding the New 2026 401(k) Limit: What It Means for You

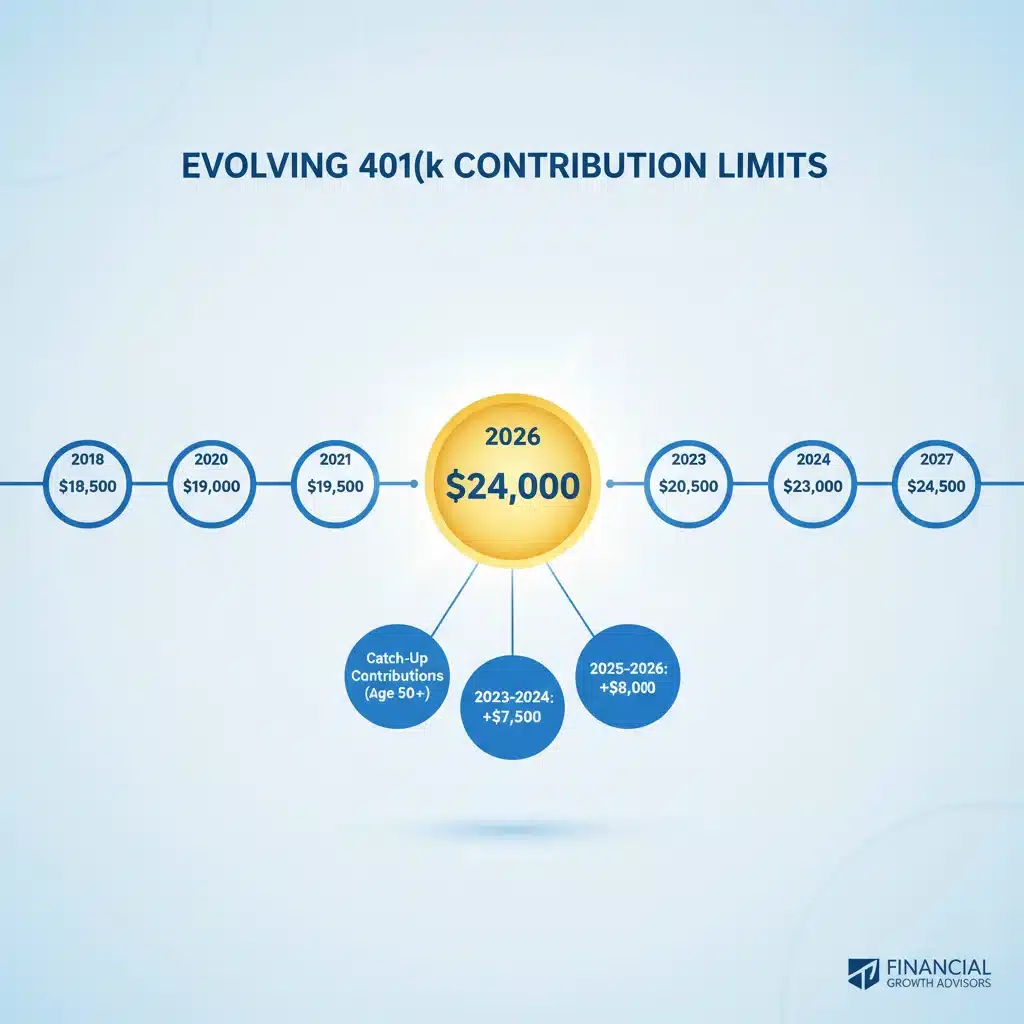

The Internal Revenue Service (IRS) periodically adjusts contribution limits for various retirement accounts to account for inflation and other economic factors. For 2026, the projected 401(k) contribution limit is set to reach $23,000. This is a significant increase from previous years and offers a greater capacity for individuals to save on a tax-advantaged basis. For many, this means a chance to significantly accelerate their retirement savings goals.

Why the Increase Matters

An increased 2026 401(k) Limit directly translates to more money you can stash away from your taxable income (for Traditional 401(k)s) or grow tax-free (for Roth 401(k)s). This allows for greater compounding over time, which is the cornerstone of successful long-term investing. The more you contribute early on, the more your money can grow, potentially leading to a much larger sum by the time you retire. For instance, contributing an extra few thousand dollars each year, compounded over 20 or 30 years, can easily translate into hundreds of thousands of dollars more in your retirement account.

Who Benefits Most?

While everyone can benefit from higher contribution limits, those with higher incomes or those nearing retirement often find these increases particularly impactful. Higher earners can shelter more of their income from current taxes, while those closer to retirement can use the increased limits to make up for lost time or to simply supercharge their final years of saving. The new 2026 401(k) Limit acts as a powerful tool for a diverse range of savers.

Strategies for Maximizing Your 2026 401(k) Contributions

Knowing the new limit is one thing; actually reaching it is another. Maximizing your 2026 401(k) Limit requires a proactive approach and often some adjustments to your financial habits. Here are several strategies to help you make the most of this opportunity:

1. Automate Your Contributions

The easiest and most effective way to hit the 2026 401(k) Limit is to set up automatic contributions from your paycheck. Divide the $23,000 (or $30,500 if you’re eligible for catch-up contributions) by the number of pay periods in a year and set your contribution percentage accordingly. This ‘set it and forget it’ approach ensures you consistently contribute without having to actively think about it each month. Many employers offer online portals where you can easily adjust your contribution percentage.

2. Prioritize the Employer Match

If your employer offers a 401(k) match, contributing at least enough to receive the full match should be your absolute first priority. An employer match is essentially free money and provides an immediate, guaranteed return on your investment. Even if you can’t hit the full 2026 401(k) Limit, always aim for the match. Missing out on an employer match is like leaving money on the table.

3. Increase Contributions Gradually

If contributing the full $23,000 immediately seems daunting, consider increasing your contributions gradually. For example, commit to increasing your contribution percentage by 1% or 2% each year, or whenever you receive a raise. This incremental approach makes it less noticeable in your take-home pay but adds up significantly over time. Before you know it, you might be hitting the 2026 401(k) Limit without feeling a pinch.

4. Utilize Catch-Up Contributions (Age 50 and Over)

For those aged 50 and over, the IRS allows for additional ‘catch-up’ contributions. While the exact catch-up limit for 2026 will be announced later, it typically adds several thousand dollars on top of the standard limit. For 2025, for instance, the catch-up contribution is $7,500, bringing the total potential contribution to $30,500. If you are eligible, leveraging these catch-up contributions is a powerful way to boost your savings in the years leading up to retirement, making the 2026 401(k) Limit even more impactful.

5. Review Your Budget

To free up more funds for your 401(k), take a critical look at your budget. Identify areas where you can cut back on discretionary spending. Even small adjustments – like reducing dining out, cancelling unused subscriptions, or finding cheaper alternatives for everyday expenses – can free up hundreds of dollars a month that can be redirected to your retirement account. Every dollar saved and invested towards the 2026 401(k) Limit has the potential to grow substantially over time.

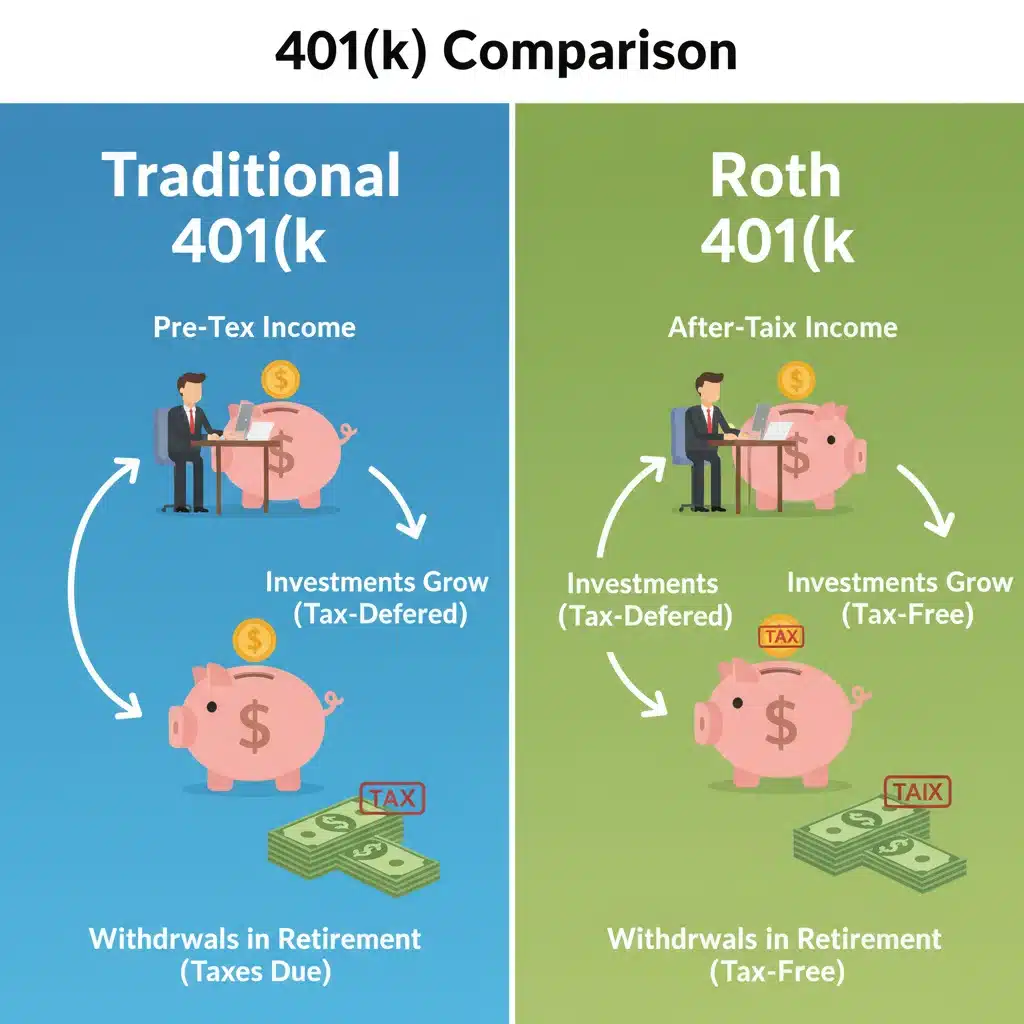

Traditional vs. Roth 401(k): Which is Right for Your 2026 Contributions?

When contributing to your 401(k), you often have a choice between a Traditional 401(k) and a Roth 401(k) (if offered by your employer). Both allow you to take advantage of the 2026 401(k) Limit, but they offer different tax benefits. Understanding these differences is key to making the best choice for your financial situation.

Traditional 401(k)

A Traditional 401(k) allows you to contribute pre-tax dollars. This means your contributions reduce your taxable income in the year you make them, leading to immediate tax savings. Your money grows tax-deferred, meaning you don’t pay taxes on the investment gains until you withdraw the money in retirement. This option is generally more beneficial if you expect to be in a lower tax bracket in retirement than you are currently.

Pros of a Traditional 401(k):

- Upfront Tax Deduction: Reduces your current taxable income.

- Tax-Deferred Growth: Your investments grow without being taxed annually.

- Potentially Lower Taxes in Retirement: If your income (and thus tax bracket) is lower in retirement.

Cons of a Traditional 401(k):

- Taxes on Withdrawals: All withdrawals in retirement are taxed as ordinary income.

- Required Minimum Distributions (RMDs): You must start taking distributions at a certain age (currently 73), whether you need the money or not.

Roth 401(k)

A Roth 401(k) allows you to contribute after-tax dollars. Your contributions do not reduce your current taxable income, so there’s no immediate tax deduction. However, your money grows tax-free, and qualified withdrawals in retirement are also tax-free. This option is generally more beneficial if you expect to be in a higher tax bracket in retirement than you are currently, or if you simply prefer the certainty of tax-free income in retirement.

Pros of a Roth 401(k):

- Tax-Free Withdrawals in Retirement: Qualified distributions are tax-free.

- Tax-Free Growth: Your investments grow without being taxed.

- No RMDs for the original owner: (Though beneficiaries may have them).

- Flexibility: Contributions can be withdrawn tax- and penalty-free at any time (though earnings cannot).

Cons of a Roth 401(k):

- No Upfront Tax Deduction: You don’t get a tax break in the year of contribution.

- Higher Current Taxable Income: Your current take-home pay might be slightly lower compared to a Traditional 401(k) if contributing the same amount.

Making the Choice for the 2026 401(k) Limit

The decision between a Traditional and Roth 401(k) depends on your individual circumstances, current income, and future tax expectations. Many financial advisors suggest a diversified approach, contributing to both pre-tax and after-tax accounts to hedge against future tax rate uncertainties. If you’re unsure, consulting with a financial planner can help you determine the best strategy for your specific situation, especially when considering the impact of the new 2026 401(k) Limit.

Beyond the 401(k): Other Retirement Savings Vehicles

While the 401(k) is a cornerstone of retirement planning, it’s often not the only account you should be utilizing. Especially when you’re maximizing your 2026 401(k) Limit, it’s wise to consider other tax-advantaged accounts to further boost your savings.

Individual Retirement Accounts (IRAs)

IRAs (Traditional and Roth) offer another avenue for tax-advantaged savings. For 2026, the IRA contribution limit is also expected to see an inflation-adjusted increase. If you’ve already maxed out your 401(k), an IRA can be a great next step. Roth IRAs, in particular, offer tax-free growth and withdrawals, and their income limitations can sometimes be bypassed through a ‘backdoor Roth IRA’ strategy for high earners.

Health Savings Accounts (HSAs)

Often dubbed the ‘triple-tax advantage’ account, an HSA is an excellent retirement savings vehicle for those with high-deductible health plans. Contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free. Once you reach age 65, you can withdraw money for any purpose without penalty, though it will be taxed as ordinary income if not used for medical expenses. This makes it a powerful complement to your 2026 401(k) Limit strategy.

Taxable Brokerage Accounts

Even after maxing out all your tax-advantaged accounts, a taxable brokerage account can play a crucial role in your retirement plan. While these accounts don’t offer the same tax benefits, they provide liquidity and flexibility. By investing in a diversified portfolio of low-cost index funds or ETFs, you can still achieve significant growth. Capital gains and dividends are typically taxed at lower rates than ordinary income, making them an efficient option for long-term growth.

Common Pitfalls to Avoid When Saving for Retirement

Even with a clear understanding of the 2026 401(k) Limit and various savings strategies, certain pitfalls can derail your retirement plans. Being aware of these can help you navigate your financial journey more smoothly.

1. Not Starting Early Enough

The power of compounding interest is immense, but it requires time. Delaying your retirement savings, even by a few years, can significantly impact your final nest egg. Start contributing as early as possible, even if it’s a small amount. Every year counts, and the new 2026 401(k) Limit provides an even stronger incentive to begin now.

2. Being Too Conservative with Investments

While it’s important to be mindful of risk, being overly conservative, especially when you’re young, can hinder growth. Stocks generally offer higher returns over the long term compared to bonds or cash. Ensure your investment allocation aligns with your risk tolerance and time horizon. As you approach retirement, you can gradually shift towards a more conservative portfolio, but don’t miss out on growth opportunities early on.

3. Cashing Out Your 401(k) When Changing Jobs

When you leave a job, you typically have options for your 401(k): leave it with the old employer, roll it over into your new employer’s plan, or roll it into an IRA. Cashing it out should almost always be avoided. Not only will you face income taxes on the distribution, but you’ll also likely incur a 10% early withdrawal penalty if you’re under 59½. This can severely set back your progress towards reaching the 2026 401(k) Limit and your overall retirement goals.

4. Forgetting About Inflation

The cost of living will undoubtedly be higher in retirement than it is today. While the 2026 401(k) Limit helps, it’s crucial to factor inflation into your retirement projections. Aim to save enough not just to cover today’s expenses, but to cover the inflated cost of those same expenses decades from now. This means your investments need to grow at a rate that outpaces inflation.

5. Not Rebalancing Your Portfolio

Over time, the asset allocation in your 401(k) can drift from your target due to market fluctuations. Periodically rebalancing your portfolio (typically once a year) helps you maintain your desired risk level and ensures you’re not over-exposed to certain asset classes. This simple practice can help keep your retirement plan on track, especially as you strive to maximize the 2026 401(k) Limit.

The Role of Financial Planning in Leveraging the 2026 401(k) Limit

While this article provides a comprehensive overview, personal financial planning is a nuanced process. A qualified financial advisor can offer tailored guidance, helping you optimize your savings strategy to take full advantage of the 2026 401(k) Limit and beyond.

Personalized Investment Advice

A financial planner can help you select appropriate investments within your 401(k) that align with your risk tolerance, financial goals, and time horizon. They can also help you diversify your portfolio across different asset classes to mitigate risk and maximize returns, ensuring that your contributions towards the 2026 401(k) Limit are working as hard as possible for you.

Tax Optimization Strategies

Beyond the choice between Traditional and Roth 401(k)s, there are other tax strategies that can enhance your retirement savings. A planner can help you understand tax-loss harvesting, efficient withdrawal strategies in retirement, and how different account types interact to create a tax-efficient overall financial plan. This comprehensive approach ensures you’re not just saving, but saving smartly, particularly with the new 2026 401(k) Limit.

Estate Planning Integration

Retirement planning doesn’t end with accumulating wealth; it also involves planning for its distribution. A financial advisor can integrate your retirement savings with your broader estate plan, ensuring your assets are passed on according to your wishes and with minimal tax implications. This holistic view is crucial for long-term financial security.

Conclusion: Secure Your Future with the 2026 401(k) Limit

The projected increase of the 2026 401(k) Limit to $23,000 is a significant development that offers a powerful opportunity for individuals to accelerate their retirement savings. By understanding this new limit, implementing strategic contribution methods, and making informed decisions about your account types, you can significantly enhance your financial future.

Remember to automate your savings, prioritize any employer match, and utilize catch-up contributions if eligible. Carefully consider whether a Traditional or Roth 401(k) aligns better with your tax outlook, and don’t overlook other valuable savings vehicles like IRAs and HSAs. By avoiding common pitfalls and considering professional financial guidance, you can build a robust retirement portfolio that stands the test of time.

Start planning today to take full advantage of the 2026 401(k) Limit and pave the way for a secure and comfortable retirement. Your future self will thank you.

in 2025: Data-Driven Retirement Comparison")