Federal Employee Benefits 2026: A Comprehensive Comparison of FEHB and FERS Updates

As federal employees, understanding your benefits is paramount to securing your financial future and ensuring your well-being. The landscape of federal benefits is dynamic, with periodic adjustments and legislative changes impacting everything from healthcare to retirement. With 2026 on the horizon, it’s crucial to delve into the anticipated updates for two of the most significant programs: the Federal Employees Health Benefits (FEHB) program and the Federal Employees Retirement System (FERS).

This comprehensive guide aims to provide a detailed comparison of the expected changes to federal benefits 2026, offering insights and actionable advice to help you navigate these important decisions. Whether you are a new federal hire, nearing retirement, or somewhere in between, staying informed about these updates is essential for optimizing your personal benefits strategy.

Understanding the Pillars of Federal Benefits: FEHB and FERS

Before we dive into the specifics of federal benefits 2026, let’s briefly recap the foundational aspects of FEHB and FERS. These two programs form the bedrock of a federal employee’s compensation package beyond their salary.

The Federal Employees Health Benefits (FEHB) Program

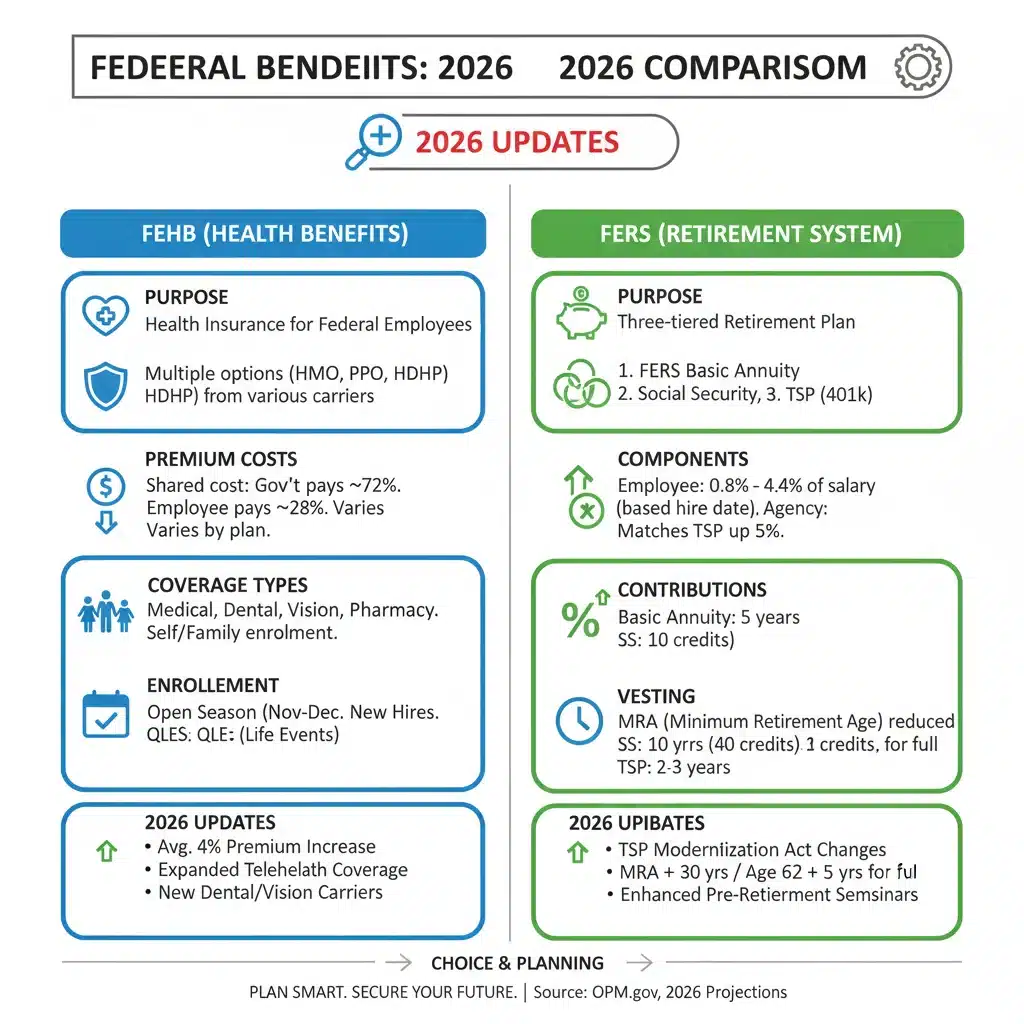

The FEHB program is one of the most significant benefits offered to federal employees, retirees, and their families. It provides a wide selection of health plans, allowing individuals to choose the option that best suits their needs and budget. Managed by the U.S. Office of Personnel Management (OPM), FEHB plans are typically offered by private insurance carriers, but they must meet OPM’s requirements. This competitive environment generally leads to a robust selection of plans, including Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and High Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs).

Key features of FEHB include:

- Extensive Choice: A vast array of plans available across the country.

- Government Contribution: The government pays a substantial portion of the premiums, typically around 72% of the average premium for all plans, but not more than 75% of the premium for any specific plan.

- No Waiting Periods: Coverage generally begins immediately upon enrollment.

- Coverage for Dependents: Spouses and eligible children can be covered.

- Continuation into Retirement: Eligibility to continue FEHB coverage into retirement, provided certain conditions are met, is a major advantage.

The Federal Employees Retirement System (FERS)

FERS is a three-tiered retirement plan for federal employees hired after December 31, 1983. It comprises three main components:

- Basic Benefit Plan: A defined benefit plan, similar to a traditional pension, where the annuity amount is determined by years of service and high-three average salary.

- Social Security: Federal employees under FERS also contribute to and receive benefits from Social Security.

- Thrift Savings Plan (TSP): A defined contribution plan similar to a 401(k), offering a variety of investment options. The government automatically contributes 1% of your basic pay to your TSP account and matches employee contributions up to an additional 4%, for a total of 5% government contribution.

FERS is designed to provide a comprehensive retirement income stream from these three sources, offering both stability through the basic benefit and flexibility through the TSP. Understanding how these components interact is vital for effective retirement planning, especially with potential adjustments to federal benefits 2026.

Anticipated Updates and Changes for Federal Benefits 2026

While definitive legislation and OPM directives for 2026 are still evolving, we can anticipate certain areas where changes are most likely to occur. These predictions are based on historical trends, current economic conditions, and ongoing legislative discussions surrounding federal benefits. Staying informed about these potential shifts is crucial for federal employees planning for the future.

FEHB Program: What to Watch For in 2026

The FEHB program undergoes annual adjustments, but 2026 could bring more significant structural or cost-sharing changes. Here are some key areas to monitor:

1. Premium Increases and Government Contribution Levels

It’s almost an annual certainty that FEHB premiums will see some level of increase. Factors influencing this include rising healthcare costs, inflation, and utilization rates. What’s critically important for federal employees is how these increases are shared between the government and the enrollee. Any shift in the government’s contribution formula could significantly impact out-of-pocket costs. For federal benefits 2026, watch for:

- Overall Premium Trends: Expect a continued upward trajectory, albeit hopefully moderated.

- Government Share Adjustment: Any legislative proposals to alter the government’s percentage contribution could have a substantial effect on your monthly premiums. Even a small percentage change can translate to hundreds of dollars annually.

- Plan-Specific Variations: Some plans may experience larger or smaller increases based on their claims experience and administrative costs.

2. Changes to Plan Offerings and Benefits

Each year, OPM reviews the plans offered and their benefits. For federal benefits 2026, we might see:

- Introduction of New Plans: New carriers or new types of plans (e.g., more specialized HDHPs or HMOs) may enter the market.

- Consolidation or Discontinuation of Plans: Less popular or less competitive plans might be phased out.

- Benefit Enhancements or Reductions: Plans may adjust their coverage for specific services (e.g., mental health, prescription drugs, telehealth) to comply with new mandates or to manage costs. For instance, there’s an ongoing focus on mental health parity, which could lead to further enhancements in mental health and substance abuse coverage.

- Telehealth Expansion: The increased adoption of telehealth services since the pandemic may lead to more permanent and robust telehealth benefit structures across all plans.

3. Focus on Wellness and Preventive Care

There’s a growing emphasis on preventive care and wellness programs to manage long-term healthcare costs. Federal benefits 2026 might see:

- Expanded Wellness Incentives: More plans could offer incentives for healthy behaviors, such as gym memberships, health assessments, or participation in chronic disease management programs.

- Enhanced Preventive Services: A broader range of preventive screenings and vaccinations might be fully covered, without cost-sharing.

FERS Program: Key Considerations for 2026

While FERS is a more stable system, changes can occur, particularly concerning contributions, annuities, and the Thrift Savings Plan. Here’s what federal employees should be aware of regarding federal benefits 2026:

1. Employee Contribution Rates

For employees hired under FERS-Revised Annuity Employee (FERS-RAE) and FERS-Further Revised Annuity Employee (FERS-FRAE), employee contribution rates to the basic benefit plan are significantly higher than for original FERS employees. While no immediate changes are anticipated for these rates, legislative discussions can always arise, especially concerning budget constraints. Any proposal to alter these rates for new hires or existing employees would be a major development for federal benefits 2026.

2. Thrift Savings Plan (TSP) Updates

The TSP is continually evolving to offer more flexibility and investment options. For federal benefits 2026, potential changes could include:

- New Fund Options: The introduction of new investment funds, potentially including more diverse asset classes or ESG (Environmental, Social, and Governance) options.

- Withdrawal Flexibility: Further enhancements to post-retirement withdrawal options, making it easier for retirees to access their funds in a way that suits their financial planning.

- Technology Improvements: Ongoing upgrades to the TSP website and mobile app to improve user experience and access to account information.

3. Cost-of-Living Adjustments (COLAs) for FERS Annuities

FERS annuities are subject to COLAs, which are designed to help retirees maintain their purchasing power. These adjustments are tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). While the formula itself is unlikely to change for federal benefits 2026, the economic environment and inflation rates leading up to and during 2025 will dictate the actual COLA percentage applied in 2026. Retirees and those nearing retirement should pay close attention to inflation forecasts.

4. Early Retirement and Special Provisions

Changes to early retirement eligibility or special provisions for certain occupations (e.g., law enforcement, firefighters, air traffic controllers) are less common but can occur through legislative action. While no specific proposals are currently on the table for federal benefits 2026, it’s always prudent to monitor any legislative discussions that could impact retirement eligibility or benefit calculations for these specific groups.

Strategic Planning for Federal Employees in 2026

Navigating the potential changes to federal benefits 2026 requires a proactive and informed approach. Here’s how federal employees can strategically plan to optimize their benefits.

For FEHB: Making Informed Healthcare Choices

Open Season, typically held in November/December each year, is your annual opportunity to review and change your FEHB plan. This period will be especially critical in late 2025 for federal benefits 2026.

- Review Your Current Needs: Assess your and your family’s healthcare needs for the upcoming year. Have there been changes in health status, family size, or anticipated medical procedures?

- Compare Plan Options Diligently: Don’t just stick with your current plan out of habit. Use OPM’s Plan Comparison Tool to evaluate all available options for federal benefits 2026. Pay close attention to premiums, deductibles, co-pays, out-of-pocket maximums, and prescription drug coverage.

- Consider High Deductible Health Plans (HDHPs) with HSAs: If you’re generally healthy and can afford the higher deductible, an HDHP combined with a Health Savings Account (HSA) can be a powerful tool. HSAs offer a triple tax advantage (tax-deductible contributions, tax-free growth, tax-free withdrawals for qualified medical expenses) and can be a valuable retirement savings vehicle.

- Evaluate Network Providers: Ensure your preferred doctors, specialists, and hospitals are in-network for any plan you consider to avoid unexpected costs.

- Understand Telehealth Benefits: With increased access to telehealth, understand how different plans cover virtual visits and mental health services.

For FERS: Optimizing Your Retirement Strategy

Your FERS benefits are a long-term investment. Strategic planning for federal benefits 2026 involves maximizing your contributions and understanding your retirement timeline.

- Maximize TSP Contributions: If you’re not already, contribute at least 5% of your pay to the TSP to get the full government match. This is essentially a 5% immediate return on your investment. Consider increasing your contributions up to the IRS annual limit if financially feasible.

- Diversify TSP Investments: Regularly review your TSP asset allocation. As you approach federal benefits 2026 and beyond, ensure your investment mix aligns with your risk tolerance and retirement timeline. The Lifecycle (L) Funds are a good option for those who prefer a hands-off approach, but individual F, C, S, and G Funds offer more control.

- Understand Your Annuity Calculation: Be clear on how your FERS basic annuity is calculated (High-3 average salary x years of service x multiplier). Focus on increasing your salary and service years, especially as you near retirement, to maximize this component.

- Social Security Planning: Integrate your expected Social Security benefits into your overall retirement plan. Understand how your federal service affects your Social Security eligibility and benefit amount.

- Consider Special Retirement Supplements (SRS): If you retire before age 62, the SRS bridges the gap until Social Security eligibility. Understand its duration and potential reductions.

- Consult with a Financial Advisor: A financial advisor specializing in federal benefits can provide personalized guidance tailored to your unique situation and help you navigate the complexities of federal benefits 2026.

The Impact of Economic and Legislative Factors on Federal Benefits 2026

The broader economic and legislative environment plays a significant role in shaping federal benefits. Several factors could influence federal benefits 2026:

1. Inflation and Cost of Living

Sustained inflation can lead to higher healthcare costs, impacting FEHB premiums, and can also influence the Cost-of-Living Adjustments (COLAs) for FERS annuities. A period of high inflation might prompt discussions about adjusting the government’s contribution to FEHB to ease the burden on employees.

2. Congressional Action and Budget Debates

Federal benefits are often a topic during budget negotiations and legislative sessions. Proposals to reform or modify FEHB or FERS can emerge from various political perspectives, aiming to reduce costs, enhance benefits, or streamline administration. While major overhauls are rare, incremental changes are more common. Federal employees should monitor legislative news, particularly during election cycles and budget appropriations processes, for any discussions related to federal benefits 2026.

3. Healthcare Policy Trends

Broader national healthcare policy trends, such as efforts to control drug costs, expand access to care, or promote preventive health, can influence the design and offerings within the FEHB program. OPM often aligns FEHB plans with national best practices and legislative mandates.

Resources for Staying Informed About Federal Benefits 2026

Staying current with federal benefits 2026 requires access to reliable and official sources. Here are the primary resources federal employees should utilize:

- U.S. Office of Personnel Management (OPM): OPM is the definitive source for information on FEHB, FERS, and other federal benefits. Their website (www.opm.gov) provides detailed guides, plan comparison tools, and official announcements.

- Thrift Savings Plan (TSP): For all information related to your TSP account, investment options, and withdrawal rules, the official TSP website (www.tsp.gov) is your go-to resource.

- Your Agency’s HR/Benefits Office: Your human resources or benefits office is an invaluable resource for specific questions related to your employment and benefits eligibility. They can provide personalized assistance and direct you to relevant forms and policies.

- Federal Employee Unions and Associations: Many unions and professional associations for federal employees offer resources, seminars, and advocacy on benefits issues.

- Reputable Financial Advisors: Seek out advisors who have expertise in federal benefits to get tailored advice for your situation.

Preparing for Open Season 2025 (for 2026 Benefits)

The annual Open Season is the critical period when federal employees can make changes to their health insurance, dental, vision, and flexible spending accounts. For federal benefits 2026, Open Season will occur in late 2025. This period is not just for making changes; it’s also the time to thoroughly review your current elections and understand any new offerings or adjustments.

- Start Early: Don’t wait until the last minute. Begin reviewing the OPM materials and comparing plans as soon as they become available.

- Utilize Comparison Tools: OPM’s online tools are designed to help you compare plans side-by-side based on premiums, deductibles, and other key features.

- Attend Webinars/Info Sessions: Many agencies and OPM offer webinars or information sessions during Open Season to explain changes and answer questions.

- Consider Life Changes: Any significant life event (marriage, birth of a child, change in health status) should prompt a review of your benefits to ensure they still meet your needs.

Conclusion: Proactive Engagement with Federal Benefits 2026

The landscape of federal employee benefits, particularly FEHB and FERS, is subject to ongoing adjustments. While the specifics of federal benefits 2026 are still being finalized, a proactive approach to understanding potential changes is the best strategy for federal employees. By staying informed, diligently reviewing your options during Open Season, and strategically planning your retirement contributions, you can ensure that your benefits continue to serve your and your family’s best interests.

Remember, your federal benefits package is a significant asset. Taking the time to understand and optimize it is an investment in your financial security and overall well-being. Keep an eye on official OPM announcements and legislative developments to make the most informed decisions for federal benefits 2026 and beyond.