Student Loan Forgiveness 2026: Navigating Policy Updates for Your $50,000 Debt

The landscape of student loan debt in the United States is constantly evolving, and for millions of borrowers, the prospect of student loan forgiveness remains a topic of immense interest and financial significance. As we look towards 2026, understanding the latest policy updates and how they might impact your financial future, particularly if you’re grappling with up to $50,000 in student loan debt, is more critical than ever. This comprehensive guide aims to demystify the complex world of student loan forgiveness, providing clarity on what to expect, who qualifies, and how to strategically navigate your debt.

The journey through higher education often comes with a hefty price tag, and for many, student loans become an unavoidable reality. The sheer volume of outstanding student debt in the U.S. underscores the urgent need for effective solutions and clear communication regarding relief programs. With various proposals and policy changes continuously being discussed and implemented, staying informed is your best defense against financial uncertainty. Our focus here is on Student Loan Forgiveness 2026, examining the current state of affairs and projecting potential developments that could affect your $50,000 debt.

Understanding the Current Student Loan Forgiveness Landscape

Before delving into what 2026 might hold, it’s essential to grasp the existing mechanisms for student loan forgiveness. Several programs are currently in place, each with specific eligibility criteria and benefits. These programs are often the first line of defense for borrowers seeking relief, and understanding them is crucial for anyone with student loan debt.

Income-Driven Repayment (IDR) Plans and the SAVE Plan

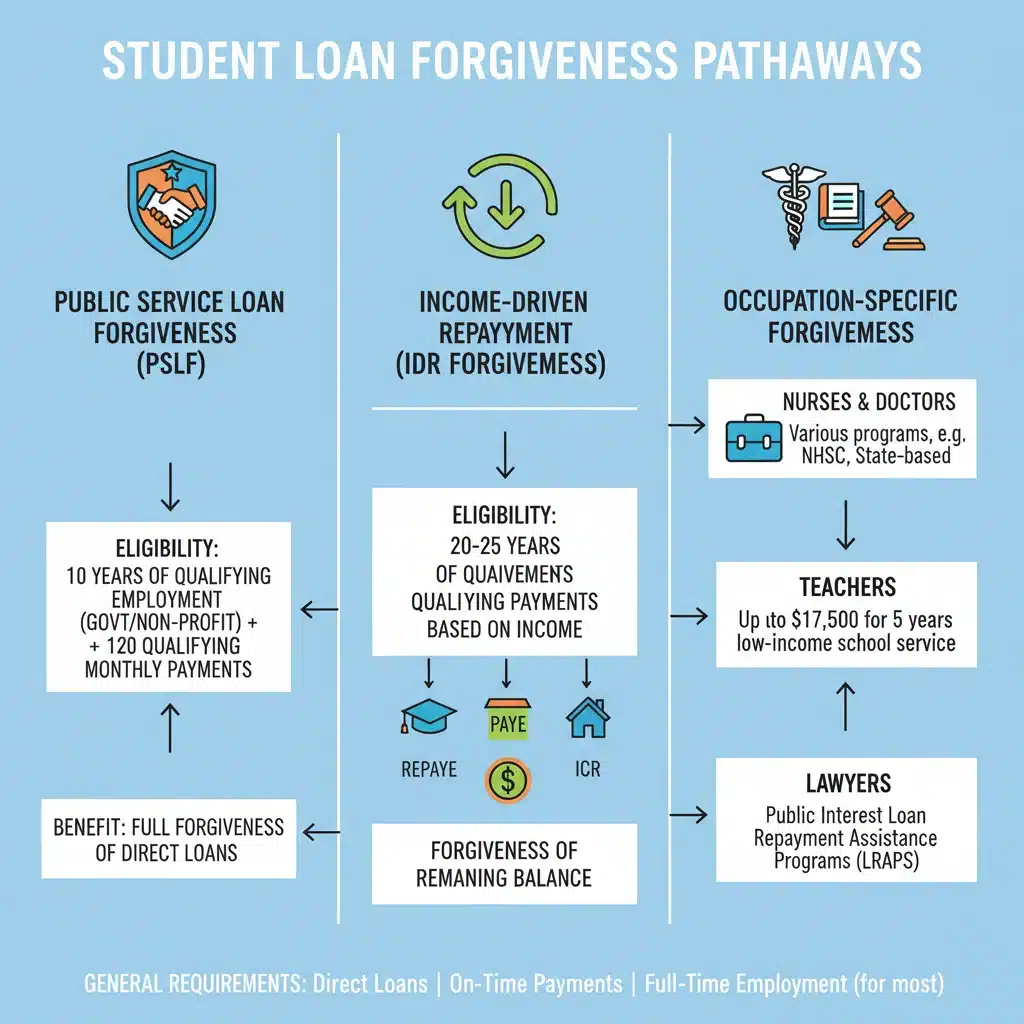

Income-Driven Repayment (IDR) plans are designed to make student loan payments more manageable by adjusting them based on a borrower’s income and family size. After a certain period of payments (typically 20 or 25 years), any remaining balance on eligible federal student loans may be forgiven. The Biden administration recently introduced the Saving on a Valuable Education (SAVE) Plan, which significantly enhances the benefits of IDR plans. The SAVE Plan offers lower monthly payments for many borrowers, especially those with lower incomes, and can lead to forgiveness much faster for some, particularly those with smaller loan balances.

Under the SAVE Plan, payments for undergraduate loans are capped at 5% of a borrower’s discretionary income, down from 10% or 15% in older IDR plans. Additionally, any unpaid interest that is not covered by the borrower’s monthly payment is waived, preventing loan balances from growing due to accruing interest. This is a monumental change, as interest capitalization has historically been a significant hurdle for borrowers trying to pay down their debt. For borrowers with original principal balances of $12,000 or less, the SAVE Plan offers loan forgiveness after just 10 years of payments. This accelerated forgiveness timeline could be a game-changer for many with $50,000 or less in debt, directly addressing the burden of smaller loan amounts more quickly.

Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness (PSLF) program is another cornerstone of federal student loan relief. It forgives the remaining balance on Direct Loans for borrowers who work full-time for a qualifying non-profit organization or government agency and have made 120 qualifying monthly payments under a qualifying repayment plan. The PSLF program has undergone significant reforms in recent years to make it more accessible and effective. The Limited PSLF Waiver, which expired in October 2022, allowed many borrowers to count previously ineligible payments towards forgiveness. While the waiver is over, ongoing efforts are being made to streamline the PSLF process and ensure more public servants can benefit from the program.

For individuals with $50,000 in student loan debt, PSLF can offer complete relief after 10 years of service, provided they meet all other criteria. It’s crucial for public service workers to ensure they are on an eligible repayment plan (such as an IDR plan) and submit their Employment Certification Form regularly to track their progress towards the 120 payments.

Teacher Loan Forgiveness

Teachers who work for five complete and consecutive academic years in a low-income school or educational service agency may be eligible for Teacher Loan Forgiveness. This program can forgive up to $17,500 for highly qualified math, science, or special education teachers, and up to $5,000 for other eligible teachers. While it doesn’t cover the entirety of a $50,000 debt, it can significantly reduce it, especially when combined with other repayment strategies.

Total and Permanent Disability (TPD) Discharge

Borrowers who are totally and permanently disabled may be eligible to have their federal student loans discharged. This discharge can be granted based on documentation from the Department of Veterans Affairs, the Social Security Administration, or a physician. This provides a vital safety net for those unable to work due to severe health conditions.

Borrower Defense to Repayment

The Borrower Defense to Repayment discharge provides relief to students whose schools engaged in misconduct, such as making false promises about job prospects or earning potential. This program has seen significant changes and expansions, offering a pathway to forgiveness for victims of predatory institutions. If your $50,000 debt stems from attending a school that engaged in such practices, you might be eligible for this type of discharge.

The "Up to $50,000" Debt Sweet Spot: Why It Matters for 2026

The figure of "up to $50,000" in student loan debt is particularly relevant because it represents a significant portion of borrowers and has been a recurring benchmark in various forgiveness proposals. While broad-based forgiveness of $50,000 per borrower has faced legal challenges, the underlying sentiment and policy goals that drove such proposals continue to influence current and future programs. The SAVE Plan, for instance, with its accelerated forgiveness for smaller loan balances, directly addresses the needs of borrowers in this range.

For those with $50,000 or less in student loan debt, the path to forgiveness or significant reduction is often more attainable through existing programs than for those with much higher balances. The impact of even partial forgiveness or reduced payments can be transformative, freeing up financial resources for other critical needs, such as housing, healthcare, or starting a family.

Projected Policy Developments and Congressional Discussions for 2026

Looking ahead to 2026, the political and economic landscape will undoubtedly continue to shape student loan policy. While a sweeping, universal forgiveness of $50,000 per borrower faces an uphill battle without new legislative action, several areas are likely to see continued attention and potential reform:

- Further Enhancements to IDR Plans: The success and impact of the SAVE Plan may lead to further refinements or expansions, potentially making IDR plans even more generous or accessible. Policymakers may seek to simplify the enrollment process or provide additional benefits to low-income borrowers.

- Targeted Forgiveness for Specific Groups: There’s ongoing discussion about expanding targeted forgiveness for specific professions beyond teachers and public servants, such as healthcare workers in underserved areas or individuals in critical STEM fields.

- Addressing "Phantom Debt": Efforts to prevent loan balances from growing due to unpaid interest, as seen in the SAVE Plan, are likely to continue. The goal is to ensure that borrowers making consistent payments see their principal balance decrease, not increase.

- Simplification of Application Processes: The complexity of applying for forgiveness programs has historically been a barrier. We can expect continued efforts to streamline applications and improve communication with borrowers, potentially through integrated online platforms.

- Congressional Action on Higher Education Act Reauthorization: The Higher Education Act, which governs federal student aid programs, is long overdue for reauthorization. Any legislative action in this area could bring significant changes to loan terms, repayment options, and forgiveness programs.

Strategies for Managing Your $50,000 Student Loan Debt

Regardless of future policy changes, proactive debt management is key. Here are strategies to consider for your $50,000 student loan debt:

1. Understand Your Loan Types

The type of loan you have (federal vs. private) significantly impacts your forgiveness options. Federal loans offer access to IDR plans, PSLF, and other federal programs. Private loans generally do not qualify for federal forgiveness programs, though some private lenders may offer their own hardship programs or refinancing options. Consolidate your federal loans into a Direct Consolidation Loan if it allows you to access better repayment or forgiveness options, but be wary of consolidating federal loans into private ones, as you’ll lose federal protections.

2. Explore Income-Driven Repayment (IDR) Plans, Especially SAVE

If you have federal student loans, immediately investigate the SAVE Plan. Calculate your potential monthly payments and see if you qualify for accelerated forgiveness. Even if you don’t receive full forgiveness, significantly reduced payments can free up your budget.

3. Check Public Service Loan Forgiveness (PSLF) Eligibility

If you work in public service, ensure you meet the PSLF criteria. Use the PSLF Help Tool to verify your employer and track your qualifying payments. Don’t wait until you’ve made 120 payments to certify your employment; do it annually to catch any issues early.

4. Consider Loan Consolidation or Refinancing

Federal Loan Consolidation: This combines multiple federal loans into a single Direct Consolidation Loan. It can simplify payments and sometimes help you qualify for certain IDR plans or PSLF if your original loans weren’t eligible. However, it can also restart your payment count towards forgiveness, so weigh the pros and cons carefully.

Private Loan Refinancing: If you have private loans or federal loans and don’t qualify for forgiveness, refinancing with a private lender might offer a lower interest rate or different payment terms. Be cautious, as refinancing federal loans into private ones means losing access to federal benefits like IDR plans and forgiveness programs.

5. Look for State-Specific or Profession-Specific Programs

Many states offer their own loan repayment assistance programs (LRAPs) for professionals in high-need areas, such as healthcare, law, or education. Research programs available in your state or for your specific profession. These can often be combined with federal programs to maximize your relief.

6. Make Extra Payments Strategically

If your financial situation allows, making extra payments can significantly reduce the total interest paid and shorten your repayment period. Focus extra payments on loans with the highest interest rates first. However, if you are actively pursuing an IDR plan with eventual forgiveness, making extra payments might not always be the most financially optimal strategy, as you’re essentially paying down a balance that might eventually be forgiven.

7. Stay Informed and Engage

Student loan policy is dynamic. Regularly check official government websites (StudentAid.gov) for the latest updates. Consider signing up for newsletters from reputable financial aid organizations. Engaging with advocacy groups can also keep you abreast of proposed changes and opportunities to voice your concerns.

Potential Challenges and Considerations for 2026

While the outlook for student loan forgiveness offers hope, several challenges and considerations remain:

- Political Volatility: Student loan policy is often a political football. Future administrations or congressional compositions could alter or even reverse existing programs.

- Economic Conditions: The broader economic climate can influence the government’s capacity and willingness to fund extensive forgiveness programs.

- Administrative Hurdles: Even with well-intentioned programs, administrative complexities can lead to delays, errors, and frustration for borrowers.

- Tax Implications: While most federal student loan forgiveness from IDR plans is currently tax-free through 2025, it’s crucial to stay informed about potential changes to the taxability of forgiven amounts beyond that date. It’s always wise to consult with a tax professional.

- Awareness and Accessibility: Many borrowers are still unaware of the programs they qualify for. Bridging this knowledge gap remains a significant challenge.

The Role of Advocacy and Borrower Voices

The continued evolution of student loan forgiveness policies is heavily influenced by advocacy groups, research organizations, and the collective voices of borrowers. Sharing your experiences, participating in surveys, and supporting organizations that champion student debt relief can contribute to shaping future policies. Lawmakers and policymakers often respond to compelling data and personal narratives that highlight the impact of student debt on individuals and the economy.

For those with $50,000 in student loan debt, understanding that you are part of a larger movement seeking equitable solutions can be empowering. The ongoing dialogue around student loan reform is not just about numbers; it’s about the financial well-being of millions of Americans and the broader economic health of the nation.

Case Studies: How Forgiveness Can Impact a $50,000 Debt

To illustrate the potential impact, let’s consider a few scenarios for a borrower with $50,000 in federal student loan debt:

Scenario 1: The Public Servant

Sarah, a social worker, has $50,000 in Direct Loans. She enrolls in an IDR plan (like SAVE) and works full-time for a qualifying non-profit. After 10 years (120 payments), her remaining balance, regardless of the amount, will be forgiven through PSLF. Her monthly payments are based on her income, making them manageable, and she doesn’t have to worry about the balance growing due to interest.

Scenario 2: The Low-Income Earner on SAVE

David, an entry-level graphic designer, has $50,000 in federal student loans. His income is relatively low, qualifying him for a $0 monthly payment under the SAVE Plan. While his loan balance is higher than the $12,000 threshold for 10-year forgiveness, his payments are affordable. Critically, his loan balance won’t grow due to unpaid interest. After 20 or 25 years (depending on his loan type), any remaining balance will be forgiven. The SAVE Plan ensures he’s not penalized for low earnings.

Scenario 3: The Teacher in a Low-Income School

Emily, a high school science teacher, has $50,000 in federal student loans. She teaches in a qualifying low-income school. After five complete and consecutive years, she applies for Teacher Loan Forgiveness and receives $17,500 in forgiveness. Her debt is reduced to $32,500. She then continues on an IDR plan, and if she stays in public service, she could potentially pursue PSLF for the remaining balance, or simply pay it down with lower IDR payments.

These examples highlight that even with $50,000 in debt, multiple pathways exist for significant relief or complete forgiveness, depending on individual circumstances and career choices.

Conclusion: Navigating Your Student Loan Future

The prospect of Student Loan Forgiveness 2026 continues to be a central theme for millions of Americans burdened by educational debt. For those with up to $50,000 in student loans, the current policy landscape, particularly with programs like the SAVE Plan and PSLF, offers tangible avenues for relief. While the future of broader forgiveness remains subject to political and legislative developments, empowering yourself with knowledge and proactive strategies is paramount.

Regularly review your loan details, understand your eligibility for various programs, and don’t hesitate to seek guidance from certified financial aid advisors or consult official government resources. Your financial well-being is directly tied to how effectively you navigate these complex policies. By staying informed, engaging with available resources, and strategically planning your repayment, you can significantly mitigate the impact of your student loan debt and pave a clearer path towards financial freedom in 2026 and beyond.